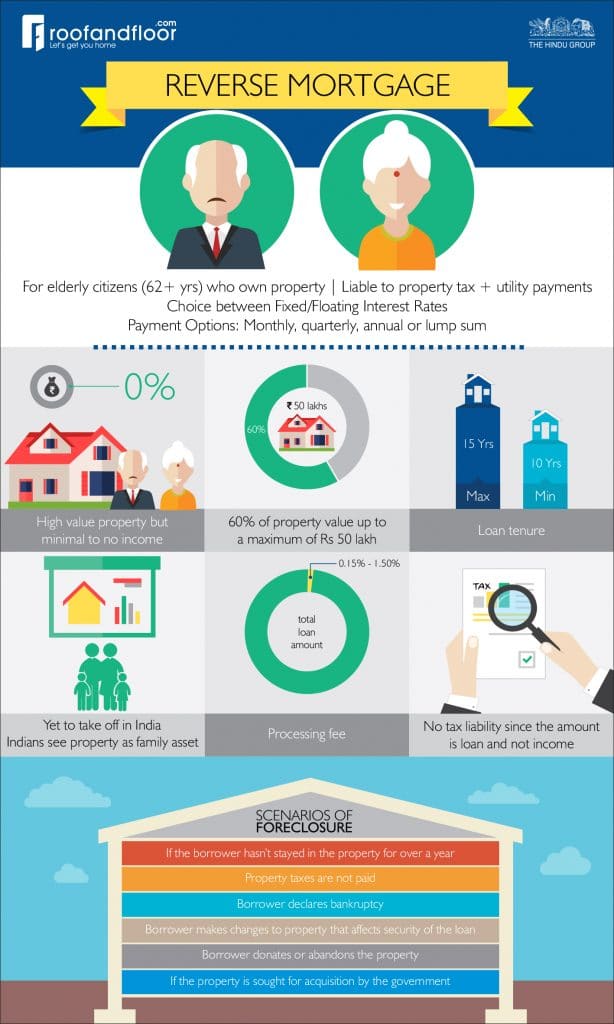

A reverse mortgage is a special type of home loan that does not require any monthly mortgage payments. Reverse Mortgages are for older citizens (62 years and older) and can be part of their retirement planning. However, they are liable for all real estate taxes applicable as well as payments to utilities.

When an individual approaches a bank for a reverse mortgage, they need to fulfill two criteria. They must be a senior citizen and must self-possess a home completely. Once the reverse mortgage is granted, the bank gives the borrower the loan amounts in EMIs over a specific period of time. Usually, reverse mortgage helps senior citizens earn a fixed periodic income. Reverse mortgages are usually repaid after the borrower’s demise. Once the borrower has passed away, legal heirs are contacted for repayment of the loan amount or sale of the property, whichever the heir chooses.

The property is generally re-evaluated once in five years by the bank. If the borrower wishes to prepay the loan amount at any period during the tenure, they can do so without facing a penalty.

When is it a good idea?

Reverse mortgage loans come across as a good way to supplement retirement income. Applying for reverse mortgage is a good idea if:

- You have a high value property but poor, unsteady source of income

- You don’t have legal heirs to pass on the property or the property isn’t high priority to your legal heirs

Yet to take off in India

These are also reasons why reverse mortgage hasn’t yet taken off in India. Indians consider owned property as a family asset to be inherited by future generations. Although reverse mortgages have existed since 2007, factors like cap on the maximum loan amount and ineffective marketing have led to people being wary about reverse mortgages. Loan amount is capped at Rs 50 lakh to Rs 1 cr which is not very lucrative, if the borrower lives in one of the metros where property prices range from over Rs 1 cr to Rs 3 cr. Also, if someone survives the term, they run the risk of losing the home if unable to repay the loan.

Scenarios of foreclosure

- If the borrower hasn’t stayed in the property for over a year

- Property taxes are not paid

- Borrower declares bankruptcy

- Borrower makes changes to property that affects security of the loan

- Borrower donates or abandons the property

- If the property is sought for acquisition by the government

When applied for apt situations, reverse mortgages can help senior citizens who own property to receive good care and support in their last years.