The world of home loan financing can be complicated. Credit scores. Down payments. Financing. There are a plethora of terms that can confuse the homebuyer from what should be a simple search for a new home.

While the average Indian homebuyer may be familiar with many of the commonly used terms in Indian real estate, one newer concept that is gaining ground is refinancing.

What’s refinancing?

Refinancing means taking a new loan to repay your old loan. Various circumstances like a change in interest rate scenario, change in income levels or moving from a fixed to floating rate of interest or vice versa are some of the reasons that warrant refinancing of your existing home loan.

How does refinancing work?

Though it is as good as taking a new loan, the process for refinancing would be slightly less cumbersome compared to taking a new home loan. In refinancing, the customer transfers his/her existing balance to a loan with a new rate of interest/tenure, either, with the existing lender or a new lender.

When do you refinance your home loan?

Substantial lower rate of interest

The Reserve Bank of India has announced a new benchmark for setting interest rates on loans called the Marginal Cost of Funds-based Lending Rate (MCLR), which is aimed at a faster transmission of rate cuts to borrowers.

If you had availed your home loan at Base Rates (the period before Apr 2016), the transmission of rate cuts is much slower and is up to the discretion of your lender. If you are stuck with home loans with a rate of interest, which is much higher than the current MCLR rate, then refinancing proves beneficial.

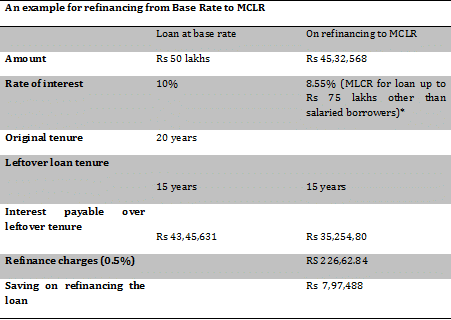

Let us show you an example to see how refinancing at a lower rate of interest proves beneficial:

Refinancing showed tremendous benefit here, as the difference in the rate of interest between the two loans was 1.45%. Experts say that only a marked difference in interest rates make refinancing worthwhile. If the difference between the existing rate and the new rate is less 0.75%, then it would not be worth refinancing your loan. If your existing loan is at a fixed rate of interest, you could also refinance to a floating rate available under MCLR rates.

Changing the loan tenure

Refinancing is not just to opt for a lower rate of interest but is an option to change the tenure of your loan too. As you know, EMI amount and the loan tenure are inversely proportional.

Suppose there is a change in income level and you can afford higher EMIs. In those cases, you could refinance your loan by opting for a lower loan tenure, thereby increasing your EMIs. By opting for a lower tenure, you decrease your overall burden of interest.

In the above example, if the loan is refinanced to reduce the tenure to 10 years (original tenure 15 years) with the outstanding principal amount at Rs 45,32,568, the EMI increases to Rs 59,898. The total interest payable over the rest of the refinanced tenure would be Rs 26,55,235. Just by decreasing the tenure of the loan by five years, the saving in interest is Rs 16,90,396 (Rs 43,45,631-Rs 26,55,235).

Poor loan servicing

Once you avail a home loan, the lender is responsible for providing you with loan and interest statements for your tax deduction and other purposes. The lender is also bound to charge your rate of interests in line with prevailing rates of interest for similar loans. If you are having trouble getting your statements or are being charged higher rates in spite of representations, you can think of moving your loan to another lender. There will be charges that you would need to bear when you switch lenders.

Refinancing is a good option available to those who would like to lower their burden of interest. Do weigh the cost of refinancing before you do so.