The year 2018 began on a promising note and ushered in a new ray of hope for the Indian realty sector. Slowly, the dust of regulatory and policy changes began to settle with the market exhibiting positive sentiments.

There’s a lot of buzz on the affordable housing front, and even on the commercial front, things are looking up.

What does this mean for you, the homebuyer?

We analysed our proprietary data for Q1 2018 (Jan-Mar) to spot trends that will define the sector in the ensuing quarters and help you make an informed home buying decision.

Highlights:

- The southern markets, including Bangalore, Chennai, and Hyderabad fared relatively well in the first quarter of 2018.

- Increased focus on completion of existing projects

- Decline in new launch supply this quarter

- Bangalore and Chennai records maximum growth in affordable housing

Bangalore realty market continues to outperform

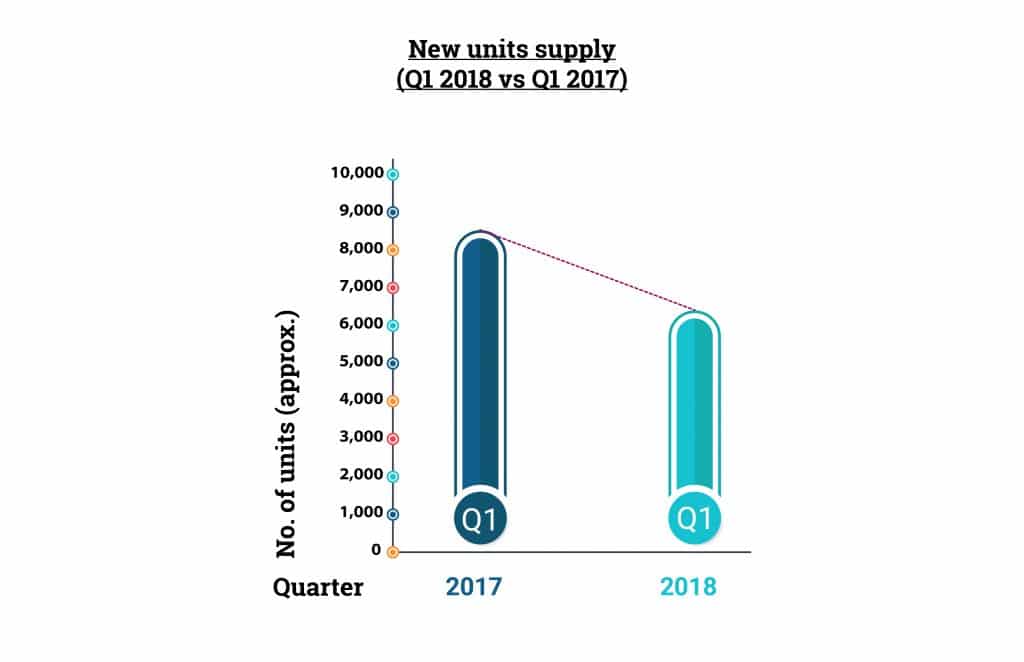

The first quarter of 2018 recorded a significant decline in the number of new units launched in all the three cities tracked. As per RoofandFloor data, new launch supply recorded a decline of nearly 29% in Q1 2018 in comparison to the corresponding quarter in 2017.

Anxious about mounting unsold inventory over the last two to three years and worried over the impact of RERA, developers are concentrating more on completion of their previously launched projects rather than launching new ones.

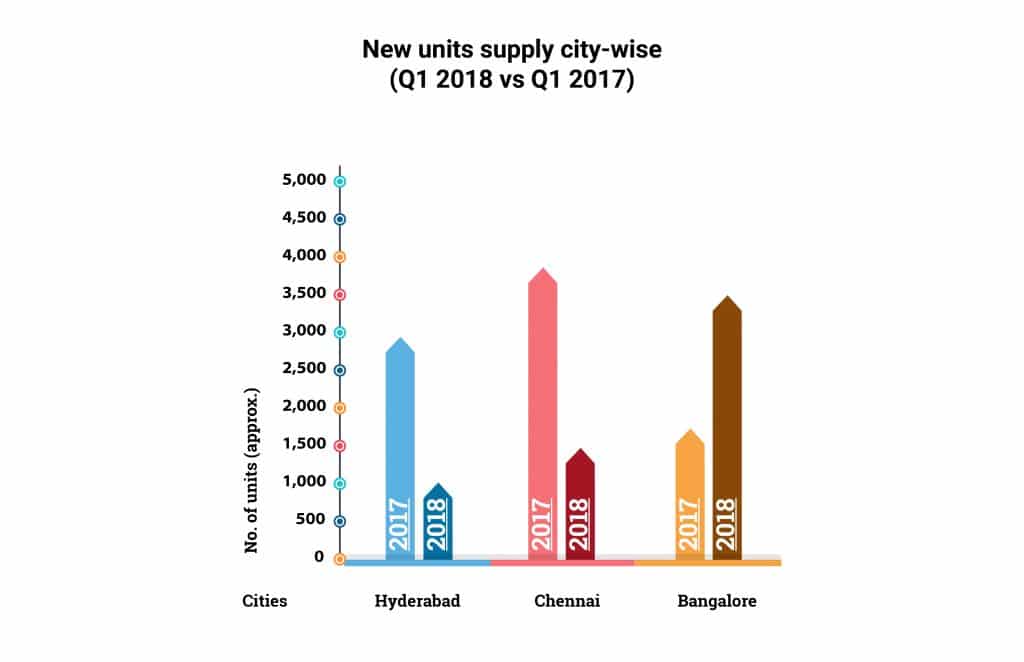

Bangalore’s realty market is showing promising growth with a 92% increase in new launch supply.

Chennai and Hyderabad recorded a sharp dip of 61% and 66% respectively.

Chennai falls in love with studio apartments

In one of the major developments in 2018, 1BHKs and studios have made an astounding entry into Chennai’s realty space. Unlike Mumbai where smaller units were always high in supply and demand, Chennai conventionally has always seen launches mostly in larger BHK configurations.

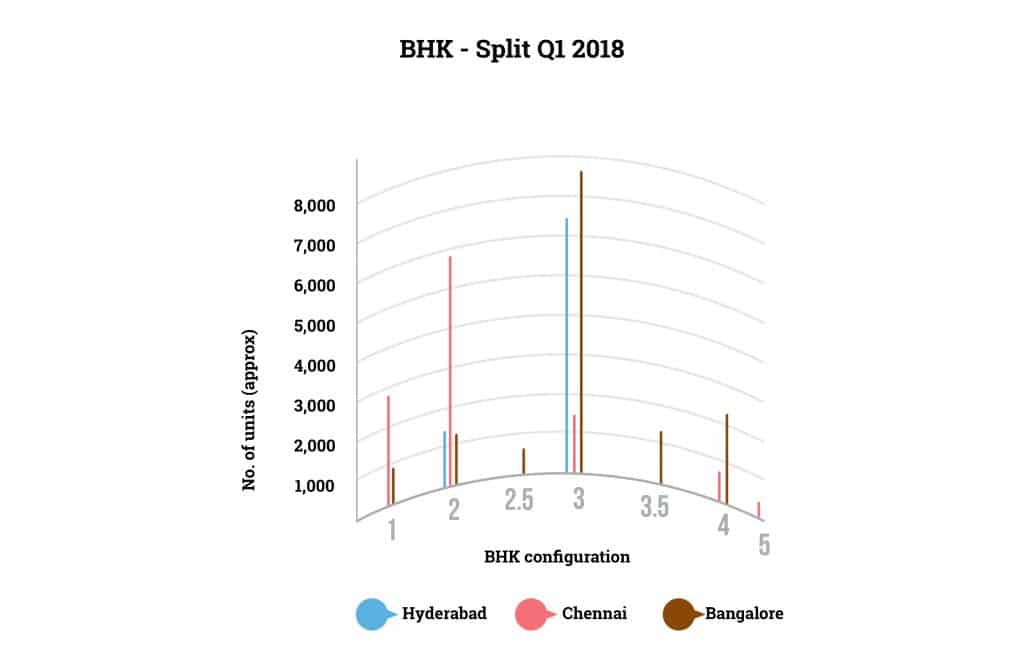

Out of the total units launched, 3BHKs have outshined the other configurations in Bangalore and Hyderabad while 2BHKs are leading the show in Chennai.

Affordable housing is the flavour of the season

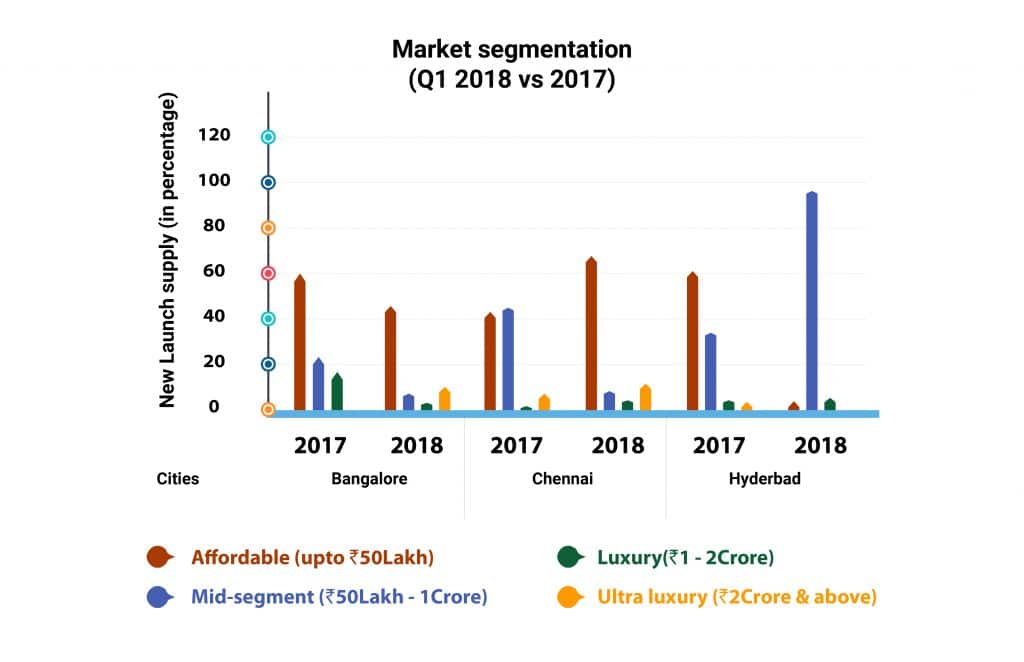

Affordable housing is the flavour of the season in Q1 2018 with significant new launches in this category in Bangalore and Chennai.

However, when compared to Q1 2017, except Chennai, the supply of affordable properties in the other two cities have recorded a significant dip.

What is interesting to note is that the luxury segment, which always ruled the roost in Chennai and Hyderabad, took the backseat this quarter. Surprisingly, Bangalore emerged stronger in this segment with nearly 49% new supply in the premium segment.

Bangalore’s red-hot real estate market

Increased commercial activity, several infra-upgrades, and improving transparency in 2017 meant that Bangalore’s real estate is much more vibrant and resilient than other cities across India.

Find out why Bangalore is a great city to invest in, according to our CEO.

In fact, the ‘Silicon Valley of India’ fared much better than its northern counterparts in terms of unsold inventory. As per market reports, in the National Capital Region or NCR, it takes about 75 months to clear unsold stock, while in Bangalore it takes about 30 months.

The IT/ITes sector ensures strong macroeconomic dynamics. And the burgeoning start-up culture in Bangalore has also set the office space ticking in the city.

As per our research, new unit supply drastically increased in Q1 2018 as against Q1 2017. Further, the affordable segment with small to mid-sized projects was dominating the property spectrum.

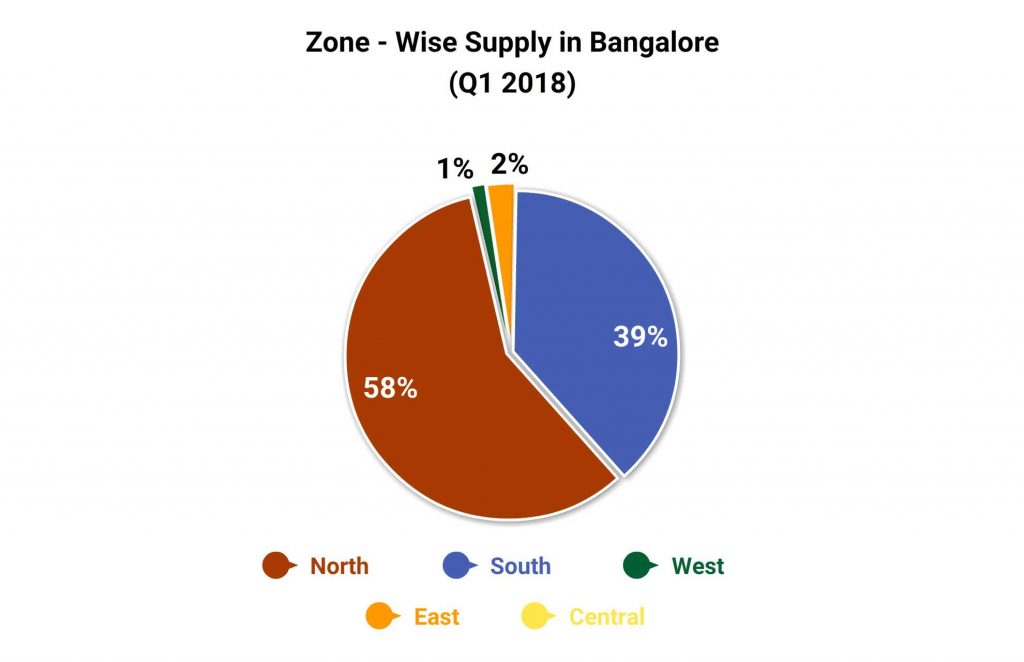

East Bangalore loses its sheen

“Ample employment opportunities, coupled with the availability of land, at a relatively lower price has transformed the skyline of the northern region in Bangalore.”

Out of 3,747 units launched in Q1 2018, nearly 58% were skewed towards North Bangalore, followed by South and East with 39% and 2% respectively.

Out of 3,747 units launched in Q1 2018, nearly 58% were skewed towards North Bangalore, followed by South and East with 39% and 2% respectively.

East Bangalore, comprising of areas like Sarjapur Road and Whitefield, that once recorded maximum supply has been overshadowed.

We attribute this to the fact that these areas already have several under-construction projects.

The top areas that saw the maximum new supply include Doddaballapur Road, Nelamangala, and Devanahalli in the North, Attibele and Off Bannerghatta Road in the South.

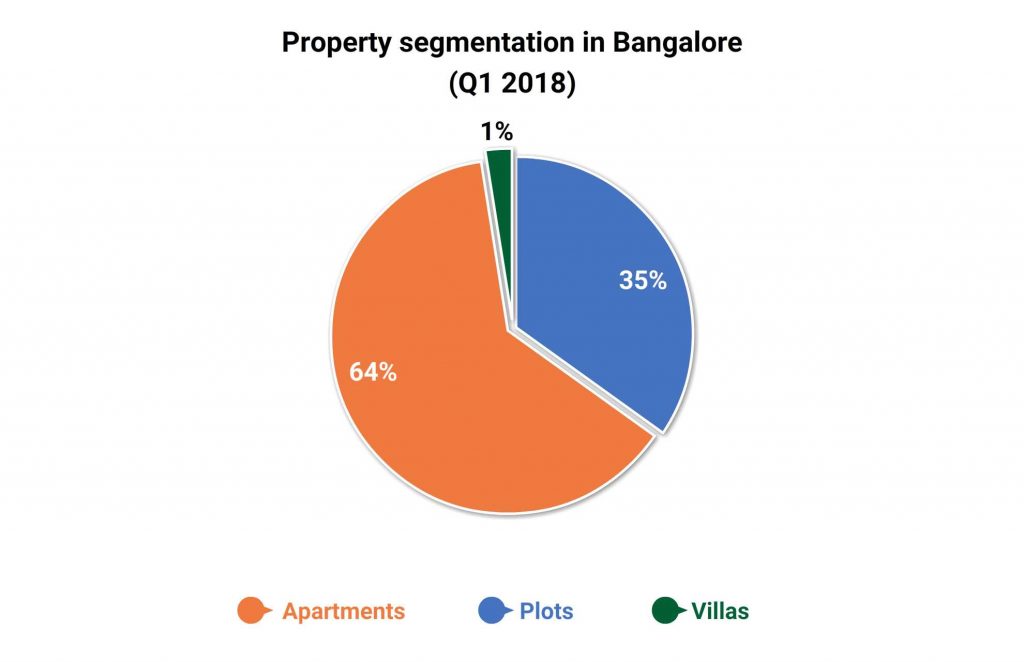

Plots make a dramatic comeback

As per property segmentation, surprisingly, plots had the clear majority in Bangalore in Q1 2018 as against the same period in 2017.

As per property segmentation, surprisingly, plots had the clear majority in Bangalore in Q1 2018 as against the same period in 2017.

Of the total units that entered the market in this quarter, a whopping 64% was plots, followed by apartments with 34%. Villas recorded a minuscule supply of 1%.

Interestingly, leading names like Shriram Properties, Godrej, and House of Hiranandani, etc. are venturing into this property segment.

Why plots?

Stringent regulations in place have forced fly-by developers to exit the market, which has created a huge opportunity for established developers.

For cash-starved developers, plots are one of the easiest ways to collect funds. The Bangalore Development Authority (BDA) has changed some of its regulations regarding plot creation.

“Earlier, developers could sell 40% of the total units on the first day, and about 30% units could only be sold after the trunk infrastructure was in place. The remaining could be sold when the full work was completed. Last year, the BDA announced that the builder could only sell when the entire physical infrastructure was in place.”

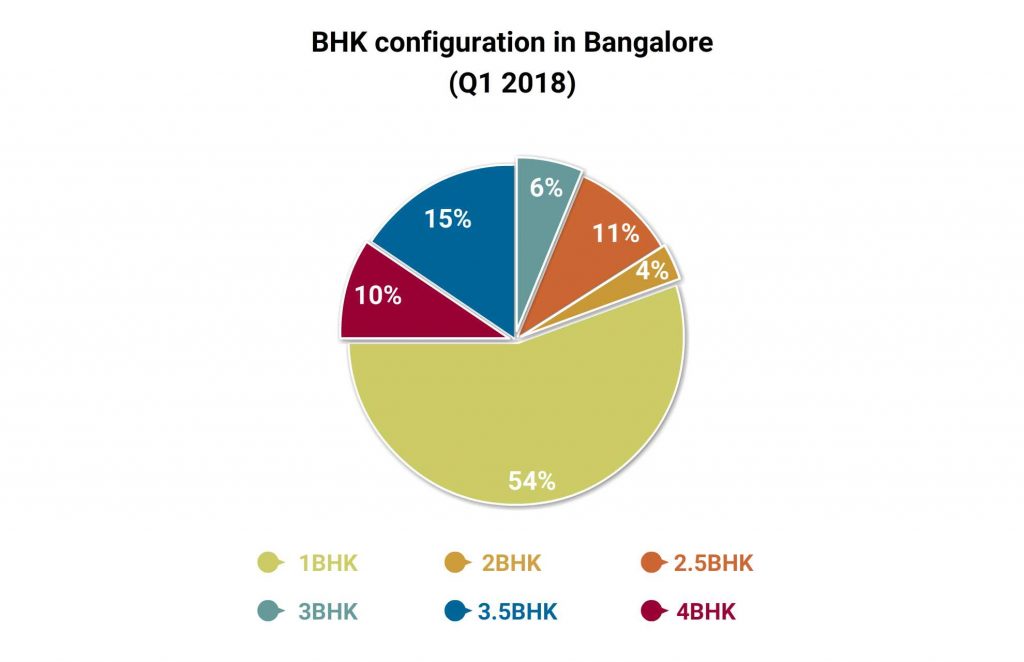

Bangalore demands more 3BHKs

Bangalore saw a good mix of units in all BHK configurations in Q1 2018. But we found that 3BHK units saw substantial supply in this quarter.

Bangalore saw a good mix of units in all BHK configurations in Q1 2018. But we found that 3BHK units saw substantial supply in this quarter.

Out of the total units launched in the city, nearly 40% were in 3BHK configuration.

The majority of these projects were skewed towards the northern part of the city, which has recorded high residential and commercial real estate activity in the last couple of years.

This larger configuration was followed by 2BHKs with 38% new supply. Interestingly, the concept of a half room has gained ground in the city. 2.5BHKs saw a supply of 5% while 3.5BHKs recorded a supply of 8%.

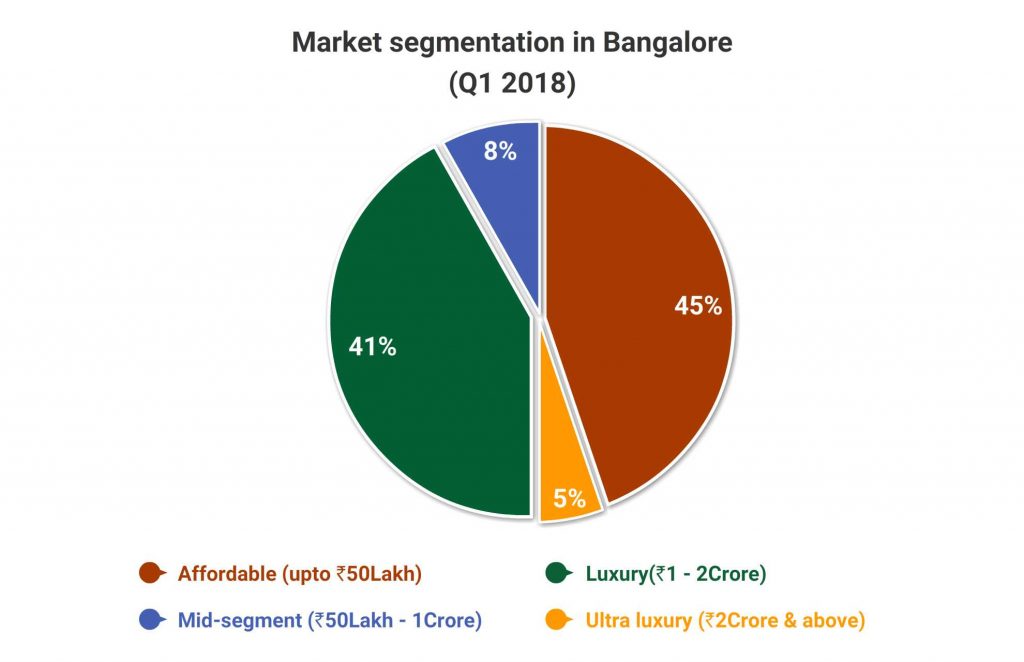

45% newly launched properties are within Rs 50 lakh

Bangalore recorded maximum supply in the affordable segment. Nearly 45% new supply was within Rs 50 Lakh.

Bangalore recorded maximum supply in the affordable segment. Nearly 45% new supply was within Rs 50 Lakh.

This can be correlated with the fact that a good number of plots entered the market in the first quarter of 2018.

Interestingly, the affordable segment was followed by the luxury and ultra-luxury segment with 41% and 8% supply respectively.

These premium units were skewed towards the northern and eastern parts of the city.

Some of the prominent projects in the luxury segment include Avani Maya, Gravity Grem Park, Aubergine Whitefield Tower, and Vivansaa Amaryllies.

Chennai’s growing market

The year 2018 has begun on a promising note with Chennai seeing a healthy supply of new units in Q1 2018. Besides the IT/ITeS sectors, the automobile, manufacturing and other ancillary industries make Chennai an attractive employment hub.

Old Mahabalipuram Road (OMR) continues to be one of the most preferred destinations for the city’s IT population, due to its proximity to various IT business parks and dedicated SEZs.

Further, while properties in the affordable segment have a clear dominance in Chennai’s market, the ultra-luxury segment is also growing at a strong pace.

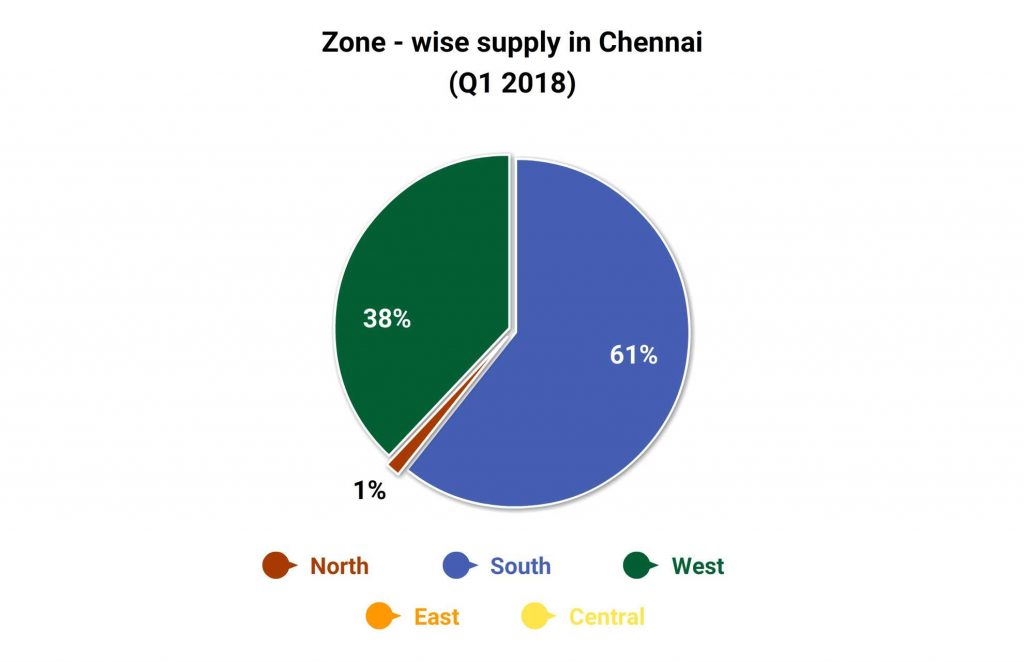

South Chennai dominates

As always, the South Zone ruled the roost with maximum new supply, followed by the West.

As always, the South Zone ruled the roost with maximum new supply, followed by the West.

Out of 1,008 units launched in Q1 2018, nearly 61% were skewed towards South Chennai, followed by West Chennai with 38%.

The top areas that saw maximum new supply in Chennai include Thalambur, Sriperumbudur, RA Puram, Avadi, and Pammal.

Of the total units, about 67% is expected to be completed by 2022. Thus, over the next three years, a healthy supply of ready-to-occupy properties will enter the Chennai market.

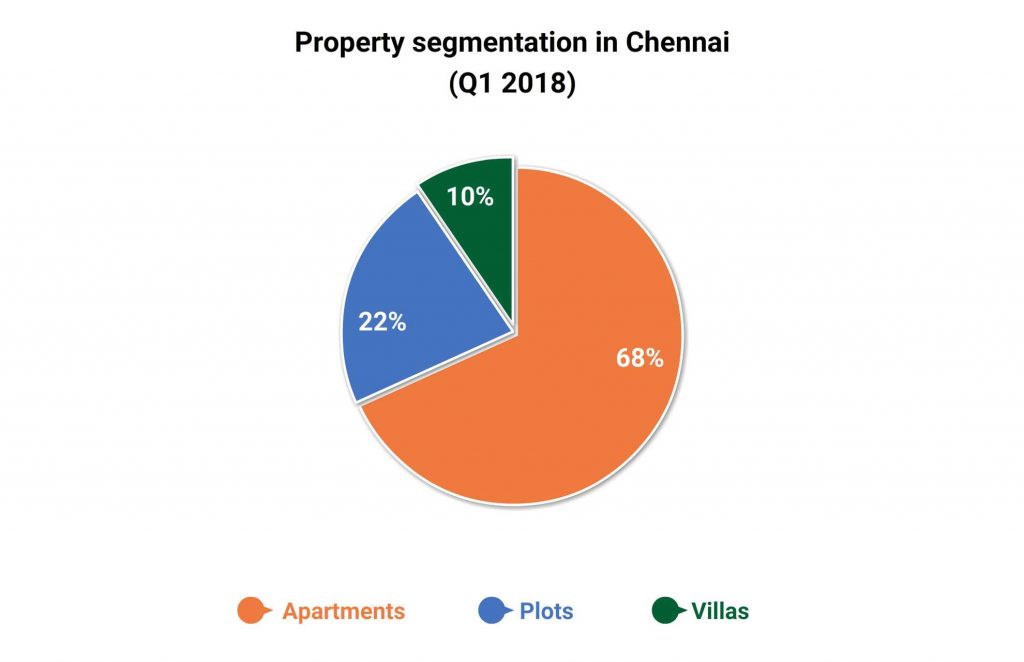

Apartment culture gains ground in Chennai

Apartments dominated the property spectrum in Chennai in Q1 2018. Of the total 1,521 new units, about 68% was apartments, followed by plots with 22%.

Villas recorded a good supply of 10%, which was largely skewed towards the southern part of the city. Villas in the 2BHK segment are gaining in popularity.

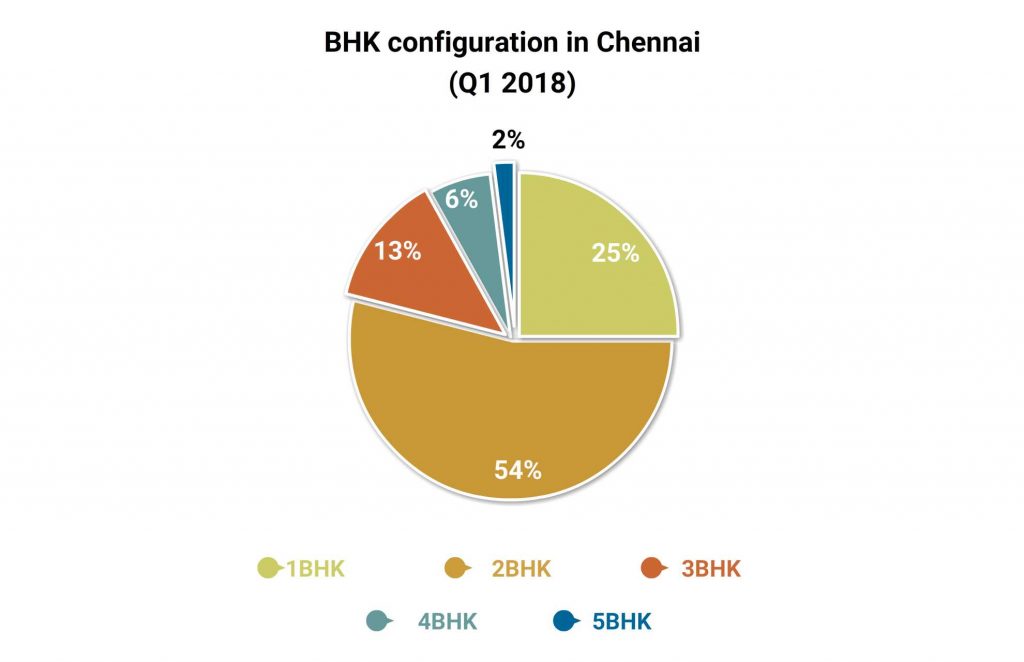

Smaller apartments slowly become popular

Chennai saw a good mix of all BHK configurations in Q1 2018. However, it was interesting to see that the city, which was largely dominated by larger BHK configurations (3 & 4BHKs), saw a rise of nearly 12% in the supply of 1BHKs and 4% in 2BHKs.

Chennai saw a good mix of all BHK configurations in Q1 2018. However, it was interesting to see that the city, which was largely dominated by larger BHK configurations (3 & 4BHKs), saw a rise of nearly 12% in the supply of 1BHKs and 4% in 2BHKs.

Out of 1,521 units launched in Q1 2018 in the city, nearly 48% of the supply was in the 2BHK configuration, closely followed by 1BHKs with a 22% supply.

These compact units were largely skewed towards the southern part of the city in markets such as Medavakkam and Thiruvanmiyur, where the demand is driven by the IT/ITeS professionals.

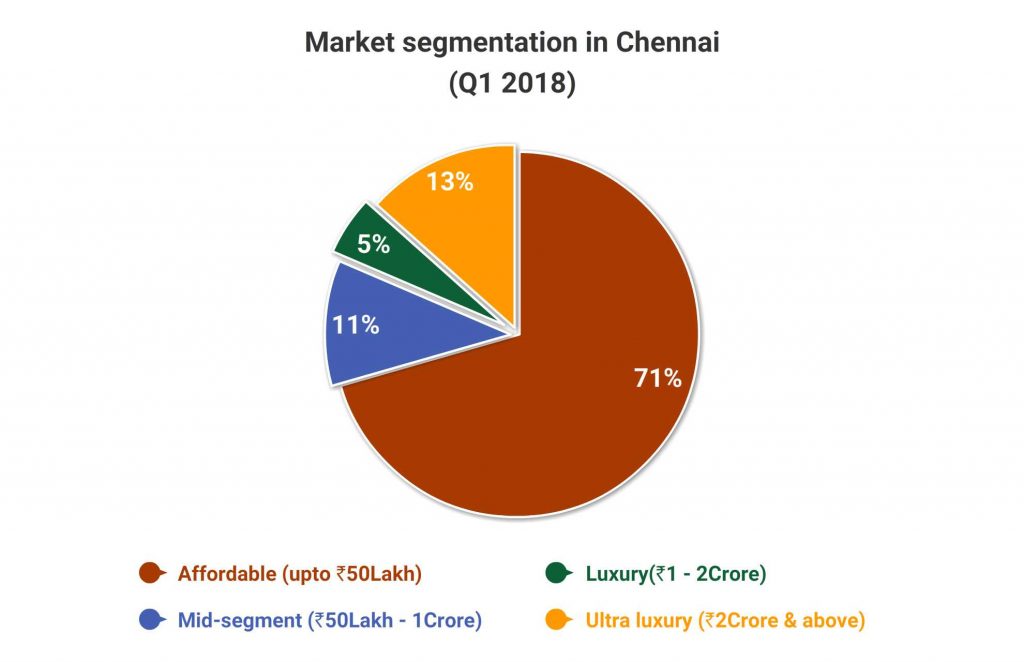

Demand for affordable homes on the rise

Like Bangalore, Chennai also recorded the maximum supply in the affordable segment.

Like Bangalore, Chennai also recorded the maximum supply in the affordable segment.

In fact, when compared to Q1 2017, the first quarter of 2018 recorded a rise of about 25% in the supply of units within Rs 50 Lakh.

This was followed by properties in the ultra-luxury segment with 13%.

Projects priced above Rs 2 Crore (ultra-luxury) were also skewed towards southern markets like RA Puram, Kottivakkam, Nanganallur, East Coast Road (ECR), and Medavakkam.

Some of the leading projects in the premium segment are Appaswamy Azure The Oceanique, Vijay Shanthi FUSO, Sri Varu Classic Brihat, Vesta’s Sundara Kamalalaya, to name a few.

Hyderabad comes into its own

Competitive property prices, sound infrastructure, and increased commercial activity has positioned Hyderabad as one of the most active southern residential markets in recent times.

Interestingly, other than the IT sector, the Hyderabad residential market is also driven by the presence of industries such as the pharmaceutical and electronics industries.

As per our research, Hyderabad has seen reasonable new supply in Q1 2018. Major real estate activity is skewed towards the western and eastern part of the city. As expected, major real estate activity was seen in the IT-centered western part of the city.

As with Bangalore, plots have attracted the attention of property investors and homebuyers here as well.

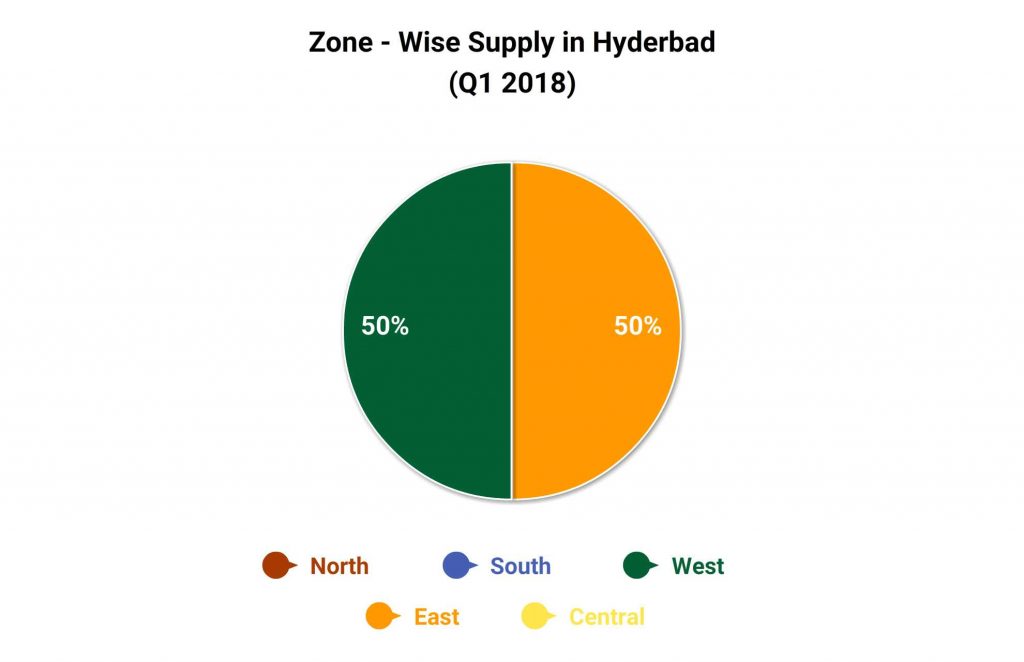

Western Hyderabad leads from the front

In Hyderabad, the majority of the new launch supply was skewed towards the western and eastern part of the city.

In Hyderabad, the majority of the new launch supply was skewed towards the western and eastern part of the city.

While the western part of the city is driven by the IT/ITeS establishments, localities in eastern Hyderabad is experiencing spillover demand from the IT zones due to increased land values.

As per our research, both these zones witnessed equal supply of new units (50% each).

Bhongir, Chandanagar, and Kismatpur were some of the top areas that recorded healthy supply in the first quarter of 2018.

Supply of plots on the upswing

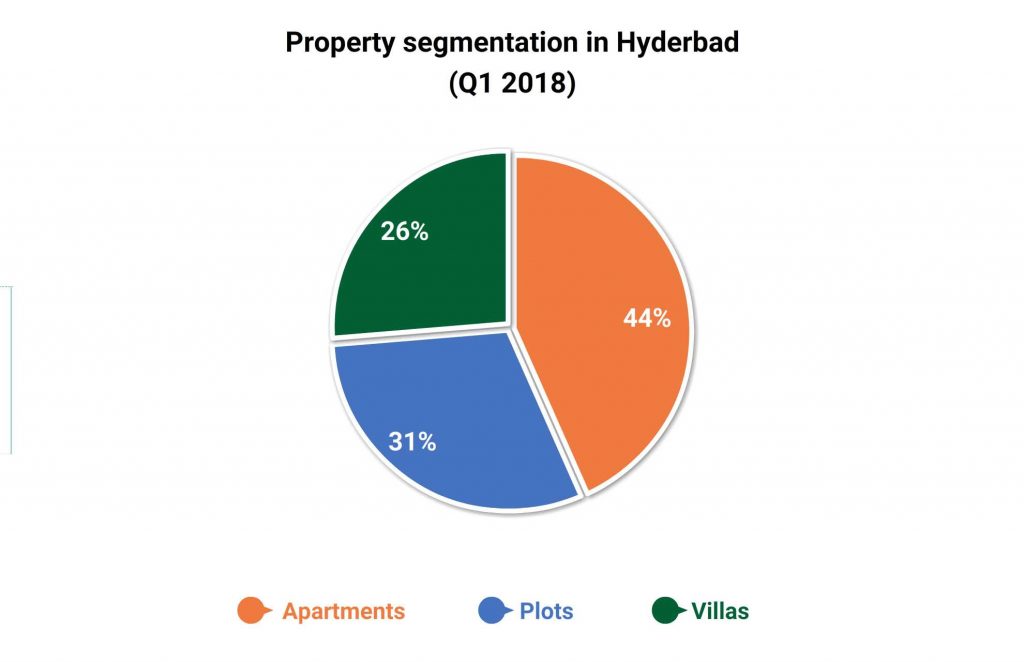

As per the property segmentation, like Bangalore and Chennai, apartments ruled the roost in Hyderabad as well.

As per the property segmentation, like Bangalore and Chennai, apartments ruled the roost in Hyderabad as well.

It is worth mentioning here that post demonetisation, buyers were cautious about investing in plots, which resulted in the low supply of this property type.

However, now with increasing demand, real estate developers are also cashing on this easy-to-liquidate property type.

Further, Hyderabad also recorded a healthy supply of villas (25%) in the 2 and 3BHK configurations.

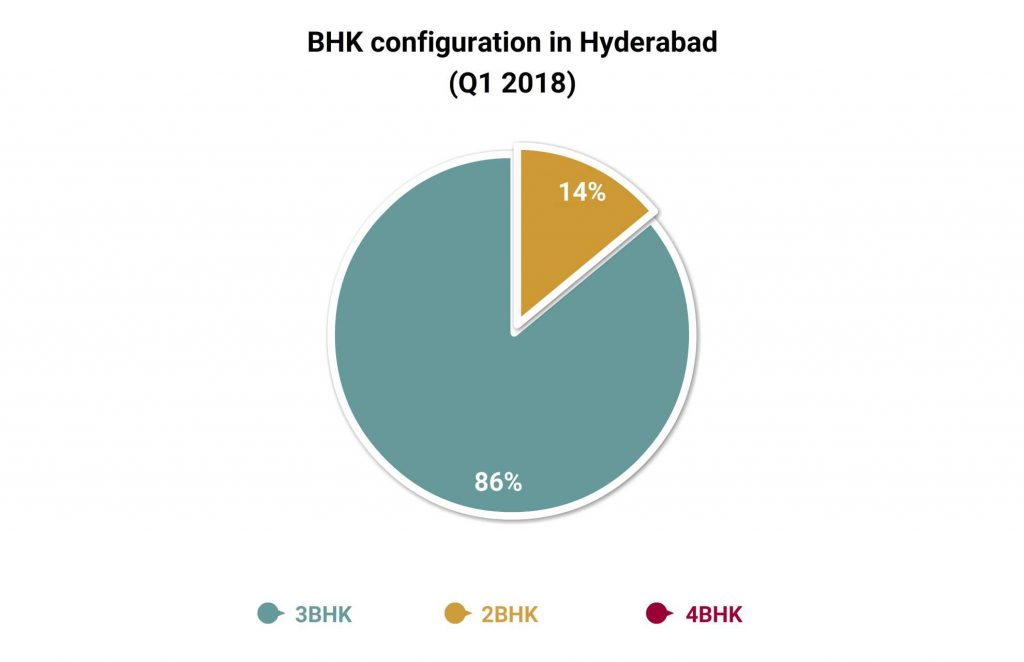

Hyderabad loves 3BHKs

Hyderabad recorded the maximum new supply in 2 and 3BHK units, with 3BHKs leading the show with 81% supply. These larger units were launched in the western part of the city in areas like Kismatpur and Narsingi.

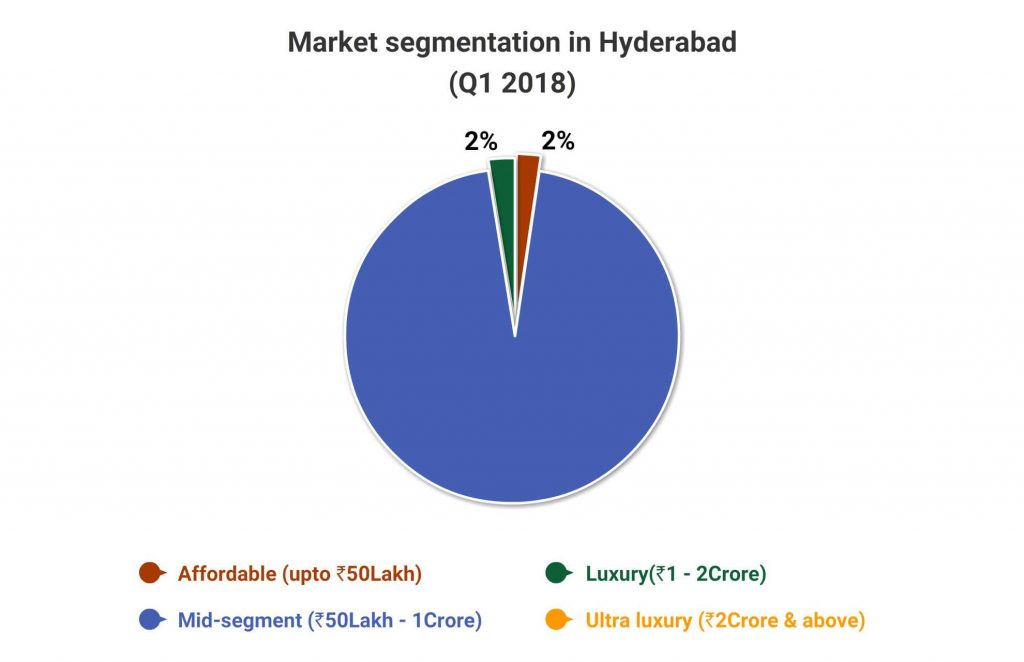

Properties in mid-range rule the roost in Hyderabad

Unlike Bangalore and Chennai, Hyderabad recorded the maximum supply in the mid-segment.

As per the data, about 96% new launched supply was in the price range of Rs 50 Lakh to Rs 1 Crore. This was followed by supply in the affordable and luxury segment with 2% each.

What’s in the future?

We peered into the crystal ball after all that heavy-duty data analysing and this is what we found.

- With decreased new launch supply, homebuyers are still going to be in the driver’s seat. Thus, it will essentially be a buyers’ market in 2018 as well.

- The demand for ready-to-occupy properties is likely to pick up pace. In fact, as developers focus on completing their existing projects, there will be ample supply of ready properties.

- The ambitious ‘Housing for All by 2022’ mission is approaching its deadline. With greater incentives for the segment, real estate majors are now looking to venture into this segment. Supply in the affordable segment (within Rs 50 Lakh) is likely to move northwards in the coming quarters.

- In terms of BHK configurations, the concept of ‘half-a-room’ seems to be gaining grounds in the realty scape of Bangalore’s market.

- Demand for plots is most likely to strengthen further as plots and layouts are easy-to-liquidate assets for both developers as well as homebuyers.

To sum it up, like the previous year, 2018 will also be a year of restricted new launch supply but improved sales velocity. It wouldn’t be wrong to say that the stage for ‘aache din’ is aptly set. It will be interesting to see how things unfold in the coming months.

Nice blog..! I really loved reading through this article. Thanks for sharing such a amazing post with us and keep blogging..

Thank you for the feedback.

Hi Nikunj,

Kudos! Great analysis!

Despite positives mentioned by you, Bangalore market also faces problems such as over-supply and ever increasing prices. To counter such issues, entrepreneurs are coming up with new solutions as well. One such attempt comes to my mind is http://www.mllion.com.

You can check them out. They might offer further insight to you. They claim to offer discounts worth millions on top of negotiated prices of property.

Thanks.

Great blog !! Gives a good perspective of the property market. I think now in 2019 the demand is more for compact, suburban apartments with affordable pricing. Main areas are like Sarjapur-Varthur, Whitefield, near International airport, etc

Thank you for such a significant resource about real estate. Keep sharing.